About FTP calculation methods

The following table summarizes three main FTP calculation methods. For more information about each, click the link for each method in the Calculation method column in the table.

| Calculation method | Used for ... | Product criteria | Product examples |

|---|---|---|---|

| Assigned Rate | Generates an FTP base rate for products that meet certain criteria (see Product criteria column). |

|

|

| Term to Maturity | Assigns rate from yield curve that matches the maturity term of fixed instruments or the number of months between rate reset dates for adjustable rate instruments. | Typically applied to instruments with a fixed balance due at maturity. |

|

| Average Term | Type of Term to Maturity. Assigns rate from the yield curve that is half of the term used for Term to Maturity. | Provided as a pricing option for adjustments but can be used for the FTP base rate if needed. | |

| Cash Flow | Matches each instrument’s principal cash flow to the rate from the appropriate term on the transfer pricing yield curve, weighted by the number of months of the cash flow. | Applied to fixed and adjustable-rate amortizing instruments. |

|

| Spread Evenly | Type of Cash Flow. Spreads the instrument’s FTP balance over the FTP term evenly without regard to amortization. | Used for products with no payment frequency, where monthly payments are assumed. |

The Assigned Rate method is generally used to generate an FTP base rate for products that do not have defined cash flows, maturity dates, and for which the interest rate is variable, has no predefined reset dates, moves with market rates, or is tied to a managed rate set by the institution. Examples include:

- Credit cards

- Lines of credit

- Demand deposits

- Instruments with variable rates

- GL only accounts, like equity, other assets, and other liabilities, are limited to using the Assigned Rate method.

- FTP adjustment rates are commonly generated using the Assigned Rate method.

This method uses key rates or blended rates to assign transfer rates. For example, direct deposit accounts (DDA) may have an FTP rate derived from 20% of an overnight rate and 80% of a two-year rate.

Assigned Rate engine processing

The price date (key rate date) used by the Assigned Rate calculation engine to select a rate is determined by the rule’s Rate Reset Flag setting:

- Monthly: Price date is the as-of-date, which is the current

YRMO ’s end of month. - Lastprice:

- If

IType = A , then the price date is the previous rate reset date if greater than the Origination/Renewal Date. It cannot be less than the origination date, or greater than the as-of-date. - If

IType = V , then the price date is the as-of-date. - If

IType = F , then the price date is the origination date.

- If

- Origination: The price date is the greater of the renewal date or the origination date defaulting to the as-of-date if no origination date or renewal date is available.

For records that do not use the Assigned Rate engine for the FTP base rate, the price date is the as-of-date. The key rate will be used by the engines as a default rate.

You can adjust the price date using day delays.

Processing warning messages

The

The following table describes the possible warning messages produced by the Assigned Rate calculation engine.

| Assigned Rate engine messages | Comment |

|---|---|

| No rule assignment. Default to Assigned Rate |

Base rate records need to have a rule assigned to them. This error will not occur when processed using the RUN FTP job. It can occur if the utilities are processed out of sequence. |

| FTP rate value is zero | Verify this is intended. You can have a key rate record that is 0. Review records in the KeyRate table. |

|

No DQA review, default FTP rate applied |

The Assigned Rate utility will process all records that have not passed DQA processing, providing default values that can subsequently be overwritten by the Term to Maturity engine. The Cash flow engine does not currently process these records. |

| DQA failure, default FTP rate applied |

Term to Maturity and Average Term methods

The Term to Maturity method assigns a rate from a yield curve that matches the maturity term of fixed instruments or the number of months between rate reset dates for adjustable rate instruments. You can modify this standard approach using the rate reset flag and the Term in Months settings in the FTP Rate Rules Setup utility.

This method is typically applied to instruments with a fixed balance due at maturity, like certificates of deposit, bonds, and some loans. It is also used to apply term-based adjustments.

The Average Term method is a variation of Term to Maturity that uses the financial instrument’s term divided by 2, which means this method assigns a rate from the yield curve that is one-half of the term used for Term to Maturity. Average Term is a pricing option for adjustments but can be used for the FTP base rate if needed.

This method uses key rates or blended rates to assign transfer rates. For example, direct deposit accounts (DDA) may have an FTP rate derived from 20% of an overnight rate and 80% of a two-year rate.

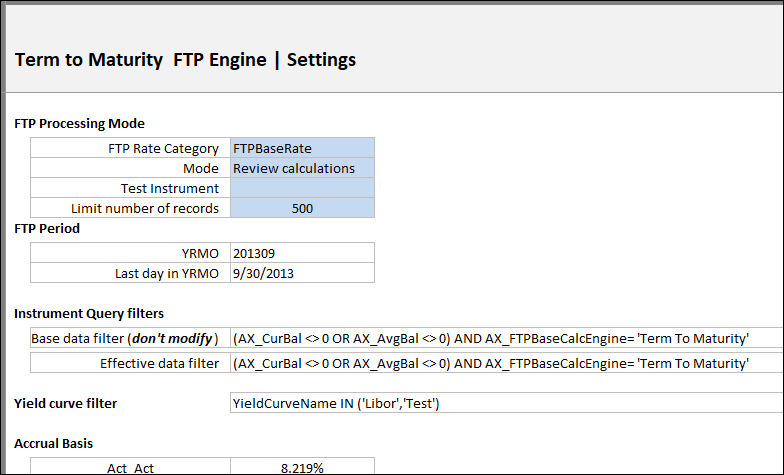

Term to Maturity processing and results

The FTPRateRules sheet loads with all rules that use the Term to Maturity engine. The sheet includes settings used by the utility. It also sets the Yield curve adjustment, which is a unique value generated for each yield curve name. The adjustment is added to every yield curve record's date to create a unique lookup value for the Match calculation that sets the lookup row for the rate index calculation. This is done because the utility cannot use an exact match to look up a yield record by name and date. Rather, the match formula must return a row that is the maximum date that is less than or equal to the Price Date, This match does not work correctly when doing an alphanumeric search, so the adjustment is used as a proxy for the curve name.

The FTPRateRules sheet also checks for the minimum date record for each yield curve. This is used to set the lower limit on the Match row lookup for each curve. It also generates a list of Yield curve names for the Yield Curve query.

The FTP rate is generated in the FTPCalc sheet. The sheet loads records from the InstModelStg table after that table has been processed by the Map FTP Rules to FTPDetailResults, Map Filtered Assignment to InstModel Stg, and Calc Assigned Rates utilities.

Warning messages

The FTP calculation engines generate warnings to report on specific results and conditions. The warnings are saved to the Message column of the FTPDetailResults table. When results are summarized and saved to the InstModelStg table, the instruments with base and assignment records that have messages will be flagged; their data is summarized and copied to the InstModelStg table, and a message will be generated for that table.

The following table describes the possible warning messages produced by the Term to Maturity calculation engine.

| Term to Maturity engine messages | Comment |

|---|---|

| Yield curve rate is 0 | Check the yield curve for 0 rates. It is possible this is from a bad data load, the interpolation did not run, or the Yield Curve Setting sheet is incorrect. |

| Default Rate | The default key rate was used for a base rate record. This happens when the yield curve rate is 0, in which case you receive a message about the yield curve rate being 0. If it is not the yield curve rate, then review the rate calculation for inconsistent dates. |

| FTP rate value is zero | If a base rate rule, the key rate had a default rate of 0. If an adjustment, either the Pricing date was before the earliest yield curve date, or the yield curve record had 0 rates. In both cases, check the yield curve records for 0 rates and the default key rate records for 0 rates. |

| Earliest yield curve date used | This is a warning when a base rate has a Pricing date that is older than the earliest yield curve record. This may not be a problem, but if intentional it may be better to have a default yield curve record that is earlier than oldest origination date to avoid this warning. |

| Unlike the Cash Flow engine, the Term to Maturity engine does not limit records to ones that passed DQA. If these messages have been passed to the FTPDetailResults engine they should be viewed as more informational than as warnings or errors because they are only saved if other issues have not been encountered. We recommended that you review records that failed DQA to validate the rates that were generated. |

Cash Flow and Spread Evenly methods

The Cash Flow FTP method matches each instrument’s principal cash flow to the rate from the appropriate term on the transfer pricing yield curve, weighted by the number of months of the cash flow. This method is commonly applied to fixed and adjustable rate amortizing instruments.

Features of the Cash Flow method include:

- Fixed rate instruments (IType F) – the transfer prices cash flows from the amortization start date through the maturity date of the instrument. The amortization start date is the first contractual payment of principal following the origination date or renewal date.

Adjustable rate instruments (IType A) – the transfer prices cash flows between the previous rate reset date and the next rate reset date.

Will calculate prepayments using CPR Constant Prepayment Rate. A type of prepayment rate., PSA Public Securities Administration. A type of prepayment rate. or SMM Single monthly mortality. A type of prepayment rate. rates.

Alternate Payment Schedules – Axiom’s Cash Flow method can transfer price customized principal payment schedules at an instrument level. Alternate Payment Schedules are stored in the AlternatePaymentSchedule table. When processed, the Cash Flow FTP engine queries the AlternatePaymentSchedule table. If a given instrument has an APSFlag = 1, then the cash flow FTP engine will defer to the payment amounts and dates of the matching alternate payment schedule table records.

The Spread Evenly method is a variation of Cash Flow. This method calculates the FTP rate using the same principal weight each period (calculated as beginning balance / number of payments) instead of calculating an instrument’s contractual cash flow.

Cash Flow engine processing and results

The yield curve sheet is only loaded when the Cash Flow engine is opened, or when Multipass is initiated. YieldCurve records are only loaded for yield curves mapped to rules using the Cash flow engine.

The FTPRateRules sheet is loaded on open with the settings for all rules that use the Cash Flow engine. It also sets the yield curve adjustment, which is a unique value generated for each yield curve name. As with the Term to Maturity engine, the adjustment is added to every yield curve record’s date to create a unique lookup value for the Match calculation that sets the lookup row for the rate record used for the instrument being processed.

The FTPRateRules sheet also checks for the minimum date record for each yield curve. This is used to set the lower limit on the Match row lookup for each curve. It also generates a list of yield curve names for the yield curve query.

The Prepayment sheet is loaded on open from the prepayment table. Similar to the yield curve, prepayment rates are dated records. They contain the effective prepayment rate and type of prepayment as of a certain date. Depending on rate rule settings, the engine selects the prepayment type and rate for a prepayment record that falls on or before an instrument’s effective origination date (the renewal date if valid). The utility returns a 0% prepayment rate if there are no prepayment records on or prior to the effective origination date. Similar to the yield curve lookup formulas, the prepayment lookup uses a derived factor for each prepayment that is added to the lookup dates to provide a unique lookup range for each prepayment name.

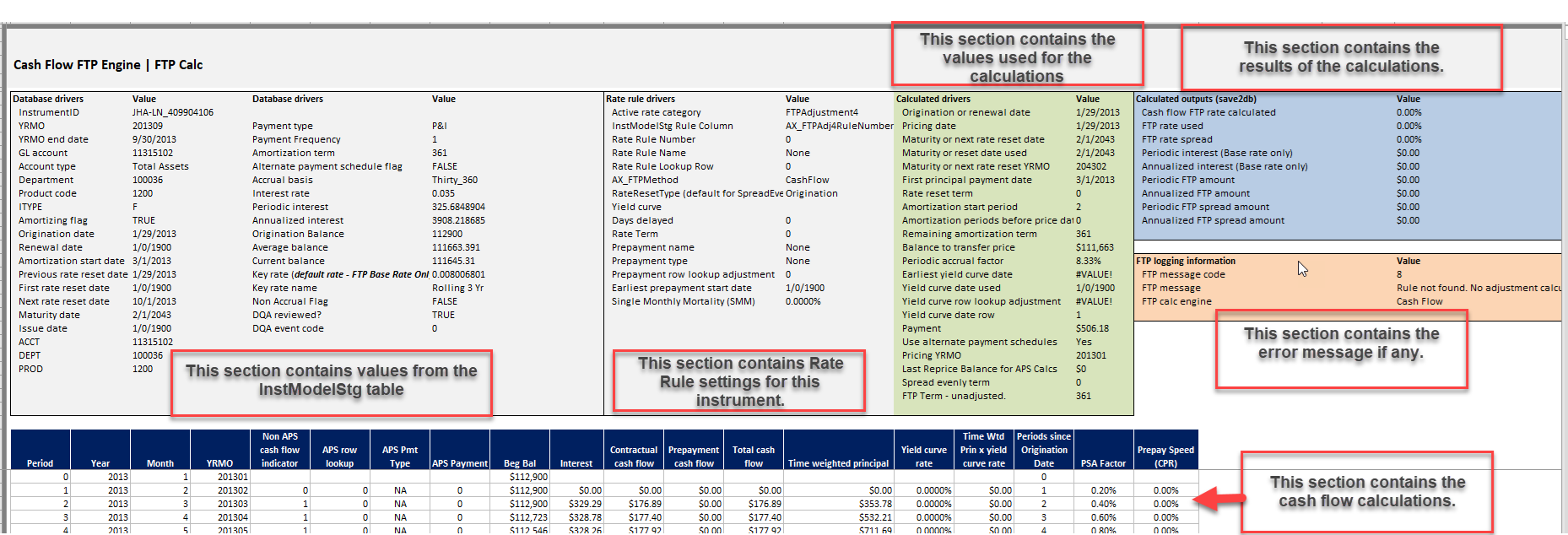

FTP data is generated in the FTPCalc sheet. Refresh the workbook to review the FTP calculation. As shown, the viewable portion of the sheet has six sections.

The sections in grey contain:

- Instrument data retrieved from either the TestInstrument sheet, or from the InstModelStg table when processing Multipass.

- Rule settings are from the FTPRateRules and Prepayments sheets.

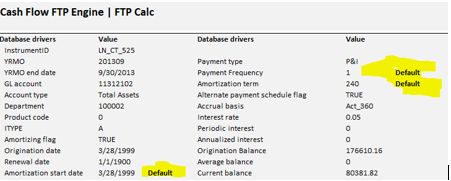

- The instrument section includes defaults for missing values that may not be populated for certain records the user wants to test using Spread Evenly:

- Amortization Term – Defaults to the difference between the amortization start date and the maturity date, or 1 if the result is 0 or negative.

- Amortization start date – Origination date or renewal date.

- Payment frequency – Defaults to 1.

Defaults are flagged when applied:

The green section contains drivers derived for the FTP calculations. Most of the settings are discussed above. Other settings of note are:

- Balance to transfer price – the balance used to calculate the current period’s FTP and, if missing, interest. It is normally the average balance but will default to the current balance if missing.

- Use alternate payment schedules – this is from the Settings sheet. If No, APS payment records will be ignored and the utility will generate payments based on loan settings. If Yes, APS settings will be used. The utility is distributed with the APS flag set to Yes.

- FTP Term – unadjusted – the calculated term used for FTP and is the term used to generate the FTP rate when the FTP rule’s Rate Term is 0. It is saved to the FTPDetailResults table along with the rule’s Rate Term.

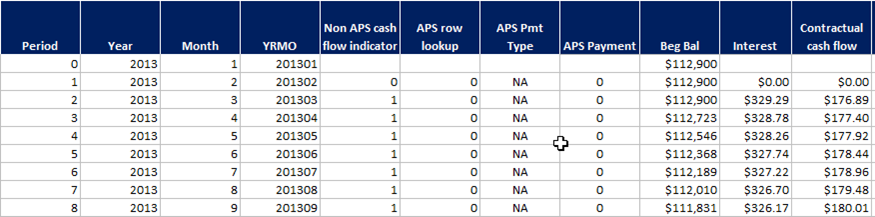

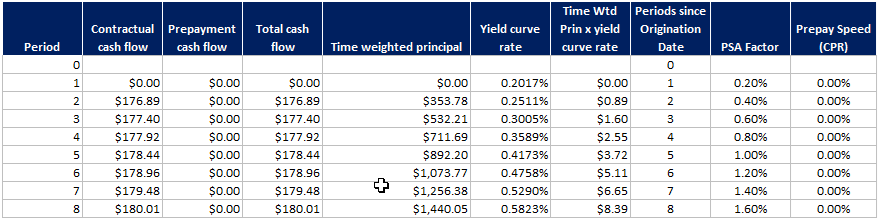

The bottom section contains the cash flow calculations used to generate the FTP rate. There are 360 monthly payment rows that are used to calculate a term X principal weighted FTP rate. The first set of calculations generate the principal portion of the payment, referred to below as Contractual cash flow. If there are APS payment records for a record, the Contractual cash flow will be calculated from them. Otherwise the Contractual cash flow will be calculated from the payment information provided by the instrument data and the Rate Rule settings.

In the example below of a fixed-rate, amortizing loan the beginning balance is the original balance of the loan. The monthly payment used to derive the Contractual cash flow is from the record. If the original balance was 0, or this was an adjustable loan, the beginning balance would be 100, and contractual payment data would be generated using standard amortization formulas.

NOTE: The principal calculations are all about weighting the yield curve rates. For amortizing loans, the weighting is not dependent on the balance used. It is dependent on the rate, the payment frequency and the number of payments.

As discussed above, the spread evenly method calculates the Contractual cash flow as the principal divided by the number of payments, thereby giving each month equal weight.

The remaining columns are used to:

- Generate prepayments if any to calculate the Total cash flow (principal)

- Calculate the Time Weighted Principal as the period X Total Cash flow

- Calculate the Time Weighted Principal and Yield Curve Rate.

The resulting FTP rate is the sum of the monthly Time Weighted Principal and Yield Curve Rate divided by the sum of the Time Weighted Principal.

Three types of prepayment rates are supported:

- SMM – single monthly mortality. The Prepay Speed is a monthly rate.

- CPR – constant prepayment rate. The Prepay Speed is an annual rate.

- PSA – public Securities Administration. A multiplier that is applied against the PSA factor column to generate the monthly Prepay Speed.

The Prepayment cash flow is calculated as:

- Prepay Speed (converted to SMM) X (Beginning Balance less the Contractual cash flow)

The conversion formula of the CPR and PSA Prepay Speeds is:

- Prepay Speed ^ 1/12

The sheet’s blue section contains the resulting values after the FTP Rate is calculated. The FTP Rate Used value will be the same as the Cash Flow FTP rate calculated unless there is a calculation error, or the resulting rate is 0. If either is the case the FTP Rate Used will be set equal to the Key Rate for Base Rate calculations, else it will default to 0.

The section in orange contains the message that will be saved with the record.